The content on this site is for educational and informational purposes only and does not constitute financial, legal, or tax advice. Results may vary based on individual circumstances, effort, and financial goals. Please consult a licensed financial professional before making any financial decisions.

The Most Expensive Mistake Families Make

Most families don't lose wealth through bad investments. They lose it through waiting.

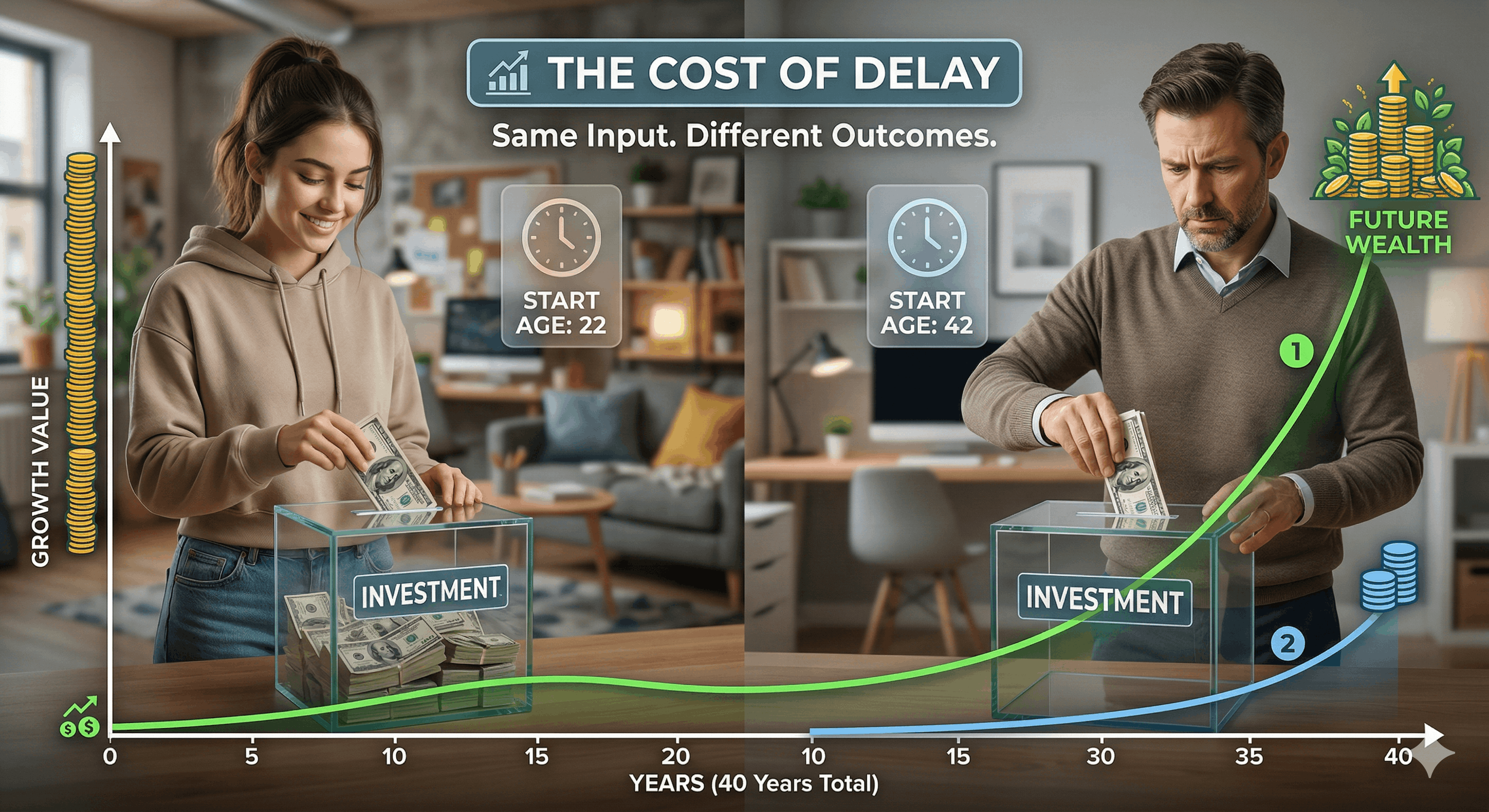

Picture two neighbors, Penny and Bill. They live on the same street. Same jobs. Same income.

Penny starts investing $200 a month at age 25. However, Bill keeps telling himself he'll start "when things settle down", and finally begins at 35.

By the time both retire at 65, the gap between their accounts isn't just noticeable. It's life-changing.

That gap — built from nothing more than a 10-year head start — is the story of compound interest.

And by the end of this post, you'll understand exactly why it happens, what the numbers actually look like, and how your family can use a free compound interest calculator to map out your own future.

What Is Compound Interest and How Does It Work?

Let's start with the basics.

There are two types of interest:

Simple interest: You earn a return only on your original deposit. Straightforward, but slow.

Compound interest: You earn a return on your original deposit AND on all the interest you've already earned. This is where the magic happens.

The formula looks like this: A = P(1 + r/n)^(nt)

(Don't worry — that's what the calculator is for.)

Where A is your final amount, P is your starting principal, r is your annual interest rate, n is how many times interest compounds per year, and t is time in years.

One more detail worth knowing: compounding frequency matters. Money that compounds monthly grows faster than money that compounds annually at the same rate. When you're comparing financial products, this is a number worth asking about.

Starting at 25 vs. 35 Is a Million-Dollar Decision

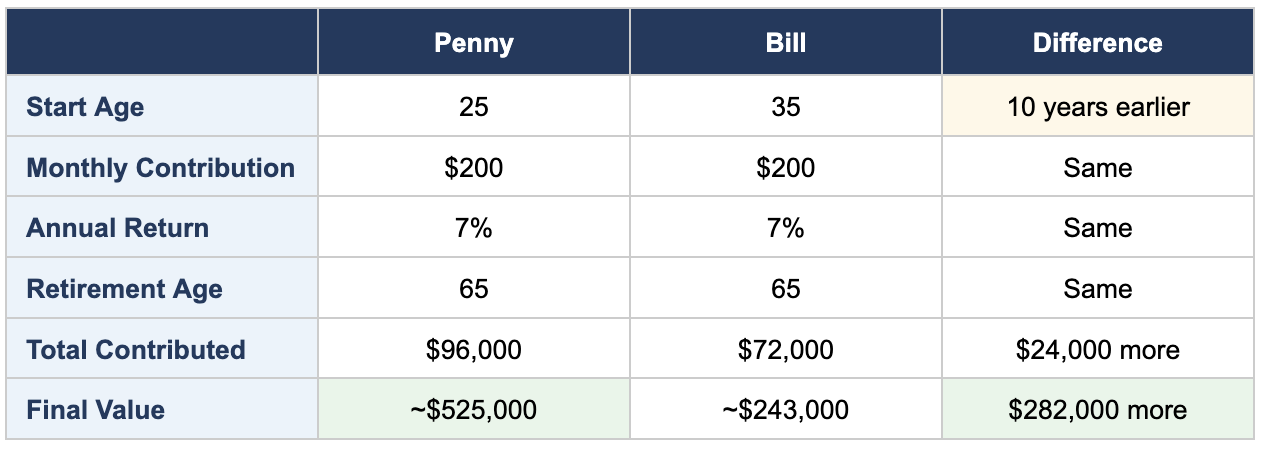

Here's where it gets real. Let's go back to those Penny and Bill, and put actual numbers on the table.

Penny contributed only $24,000 more than Investor B but ended up with $282,000 more at retirement. The extra money didn't come from a higher salary, a lucky stock pick, or a windfall. It came entirely from starting 10 years earlier and letting compound interest do the heavy lifting.

This is what financial educators mean when they say time is your most valuable asset. Every year you delay doesn't just cost you that year's contributions; it also costs you the compounding growth that would have built on every year that followed.

The Rule of 72: A Simple Mental Math Shortcut

Here's a tool that every family should know: the Rule of 72. It's a simple formula that tells you how long it takes for your money to double.

Divide 72 by your expected annual return. The result is approximately the number of years it takes to double your money.

At a 7% return: 72 ÷ 7 = about 10.3 years to double.

Here's what that means for a single $10,000 investment made at age 25:

Age 25: $10,000 invested

Age 35: ~$20,000

Age 45: ~$40,000

Age 55: ~$80,000

Age 65: ~$160,000

That same $10,000 sitting in a traditional savings account at 0.1%? It would take roughly 720 years to double.

Use our calculator to run your own Rule of 72 scenario and see what your money could become.

Real Family Scenarios

Compound interest isn't just for high earners or finance professionals. Here's what it looks like for everyday families at different stages of life.

Scenario 1: The New Parent

A couple opens an investment account the month their baby is born. They contribute $100 a month at a 7% average return.

By the time their child turns 18 and heads to college, that account has grown to roughly $43,000 — funded entirely by discipline and consistency, not a windfall or inheritance.

And if they keep contributing? It becomes the foundation of that child's financial life.

Scenario 2: The Mid-20s Professional

A 26-year-old starts investing $250 a month — less than $10 a day — and stays consistent until retirement at 65.

At a 7% average return, that single daily habit grows to approximately $685,000. No inheritance required. No six-figure salary necessary. Just time and consistency.

Scenario 3: The Late Starter Who Catches Up

Life happened. The 30s were busy — kids, a mortgage, job changes. Now it's age 40, and the question is whether it's too late. It's not.

Investing $600 a month from age 40 to 65 at 7% yields approximately $390,000 by retirement.

Not as much as starting at 25, but life-changing compared to never starting at all.

What Gets in the Way?

If compound interest is this powerful, why isn't everyone doing it? Because life is too distracting, and we're all busy.

Here are the three objections we hear most often, and the honest answers to each.

Excuse 1: "I don't have enough money to invest."

Even $50 a month compounds into something meaningful over 20–30 years. The amount matters far less than the habit. Start where you are.

Excuse 2: "The market is too risky right now."

Time in the market beats timing the market every time. Waiting for the "right moment" is one of the most expensive financial decisions a family can make. There will always be uncertainty. The families who build wealth invest through it.

Excuse 3: "I'll start when things settle down."

Things never fully settle down. There's always another reason to wait — a bill, a life event, an uncertain quarter. Waiting is not a neutral decision. Every month you delay is a month of compounding your family doesn't get back.

When you're ready to act, here are common vehicles that harness compound growth:

401(k) / IRA: Tax-advantaged accounts that let your money compound without being taxed every year.

Indexed Universal Life (IUL): Growth tied to index performance with downside protection. Your money can grow when markets rise, but it doesn't fall when the index goes negative.

Index funds: Accessible, low-cost, and diversified — a strong starting point for new investors.

The barrier to starting isn't knowledge or money. It's fear and ignorance.

Use the Calculator, Then Take the Next Step

Numbers on a page are one thing. Seeing your own family's potential is another.

Take two minutes and plug your numbers into our free Compound Interest Calculator.

All you need is three inputs:

Your starting age

How much you can contribute each year

How many years until you retire

That's it. Two minutes. And for many families, it's the moment that changes everything — not because the math is complicated, but because seeing your own number makes it real.

Your Family's Million Starts With One Decision

Remember Penny and Bill from the beginning? Same street. Same income. Same life — except for one decision made ten years apart. That decision, compounded over forty years, was worth $282,000.

Compound interest doesn't care about your zip code, your income bracket, or whether you grew up with a financial roadmap. It works the same way for everyone. Quietly. Faithfully. Every single day — as long as you give it time.

Our mission is simple: to bring Wall Street knowledge to Main Street families.

Because the strategies that build generational wealth shouldn't be reserved for people who already have it. They should belong to every family willing to learn them and start.

Book Your Free Financial Check Up

We offer free financial check-ups for families across Round Rock, Cedar Park, Pflugerville, Kyle, and the greater Austin area.

No obligation. No jargon. Just a real conversation about your family's future